Introduction: Trust Reimagined for a Digital Age

In a world increasingly defined by digital interactions, trust has emerged as both a necessity and a vulnerability. How can people, companies, or even entire economies conduct business securely without a reliable central authority? This question, once purely theoretical, has found a compelling answer in blockchain technology—a decentralized, tamper-resistant system that has swiftly grown beyond its origins in cryptocurrency to reshape industries as diverse as finance, healthcare, logistics, and governance.

Though often conflated with Bitcoin and other digital currencies, blockchain’s true promise lies deeper. At its heart, it is a technological revolution in how humans exchange value, verify information, and ensure transparency in a world where data can be copied, altered, or obscured at the click of a button.

The Basics: What Is Blockchain, Really?

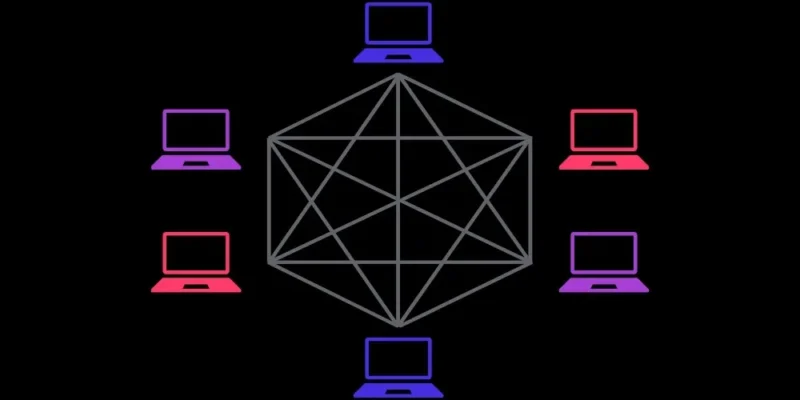

The term “blockchain” conjures images of impenetrable chains of data, and rightly so. In its simplest form, a blockchain is a distributed ledger that records transactions in blocks, which are linked together chronologically to form a continuous chain. Each block contains a bundle of transactions, a timestamp, and a cryptographic hash of the previous block—this last detail makes tampering virtually impossible.

Key characteristics of blockchain technology include:

-

Decentralization: No single entity controls the network; instead, it is maintained by a distributed community of nodes.

-

Transparency: Every transaction is recorded on a ledger accessible to all network participants.

-

Immutability: Once data is recorded, it is exceedingly difficult to alter, protecting the integrity of the information.

-

Security: Advanced cryptography safeguards transactions and prevents fraud.

Beyond Bitcoin: The Expanding Universe of Blockchain Applications

While Bitcoin brought blockchain into the public spotlight, the technology’s potential extends far beyond digital currencies. Businesses and governments alike are now exploring its capacity to solve long-standing problems of inefficiency, fraud, and opacity.

Some of the most promising use cases include:

1. Supply Chain Management

Supply chains span continents and involve countless intermediaries. Blockchain offers a transparent and traceable record of goods as they move from origin to consumer. Companies like IBM and Walmart are using blockchain to verify the authenticity of products, reduce counterfeiting, and improve food safety.

2. Financial Services

Traditional banking is bogged down by intermediaries, slow settlements, and high fees. Blockchain’s peer-to-peer architecture can dramatically reduce transaction times and costs. Smart contracts—self-executing agreements coded onto the blockchain—can automate complex processes like loan disbursements, insurance claims, and cross-border payments.

3. Healthcare Records

Patient data is scattered across hospitals, clinics, and insurance companies. Blockchain can unify these records, ensuring they are accurate, secure, and accessible only to authorized parties. By giving patients greater control over their data, the technology can help protect privacy while improving care.

4. Digital Identity

In the digital era, identity theft and data breaches are ever-present risks. Blockchain offers the possibility of self-sovereign identity—individuals hold and control their credentials on a secure ledger, presenting only what is needed and revoking access at will.

5. Voting Systems

Elections marred by fraud or inefficiency erode faith in democracy. Blockchain-based voting can increase transparency, reduce tampering, and enable secure remote voting—an idea gaining traction as societies seek more resilient electoral processes.

The Rise of Smart Contracts: Code as Law

One of blockchain’s most transformative innovations is the smart contract. Introduced by platforms like Ethereum, smart contracts are programs that automatically execute when predefined conditions are met. This eliminates the need for third-party enforcement, reduces disputes, and opens the door to entirely new forms of decentralized applications (dApps).

For example:

-

A freelance writer could receive automatic payment when an article is submitted and approved.

-

An insurance claim could trigger a payout instantly once specific conditions are verified by trusted oracles.

-

Artists could embed royalty clauses into their digital works, ensuring they earn a percentage each time the work changes hands.

Challenges and Limitations: Not a Panacea

Despite its promise, blockchain is no magic wand. It faces significant hurdles before mainstream adoption can match the fervor of its champions.

Key challenges include:

-

Scalability: Popular blockchains like Bitcoin and Ethereum handle far fewer transactions per second compared to centralized networks like Visa or Mastercard. Solutions like Layer 2 protocols and proof-of-stake consensus mechanisms are under active development to address this.

-

Energy Consumption: Proof-of-work blockchains consume enormous amounts of electricity. As the world seeks greener solutions, energy-efficient consensus methods are gaining traction.

-

Regulatory Uncertainty: Governments are still grappling with how to regulate blockchain projects without stifling innovation. Issues surrounding data privacy, taxation, and legal recognition of smart contracts remain unresolved in many jurisdictions.

-

User Experience: For everyday users, blockchain systems can be complex and intimidating. Improved interfaces and education will be crucial to unlock widespread adoption.

Blockchain’s Social Impact: A Tool for Inclusion

Amid the technical jargon and corporate experimentation, it is easy to overlook blockchain’s social potential. In regions where corruption, lack of infrastructure, or weak institutions hamper economic growth, blockchain can foster trust where none exists.

For example:

-

Land registries built on blockchain can protect property rights in countries plagued by fraudulent record-keeping.

-

Humanitarian organizations can deliver aid transparently, ensuring that resources reach intended recipients without diversion.

-

Microfinance powered by blockchain can extend affordable credit to the world’s unbanked populations.

The Road Ahead: Building the Internet of Value

Blockchain’s ultimate promise is to enable the Internet of Value—a digital ecosystem where value, like information, can flow freely, instantly, and securely. While Bitcoin may remain its most famous offspring, the broader potential of blockchain technology is only beginning to unfold.

Governments, corporations, and grassroots communities are all experimenting with this novel infrastructure. From tokenizing real estate to enabling decentralized finance (DeFi) that mirrors and surpasses traditional banking, the coming years will reveal whether blockchain’s transformative potential can be realized responsibly and sustainably.

Conclusion: A New Framework for Trust

Blockchain is more than just a technological curiosity—it is a profound reimagining of how trust can be encoded into our economic and social systems. It invites us to imagine a future where verification replaces blind faith in centralized authorities, where code enforces fairness, and where opportunity extends beyond borders and institutions.

As this invisible architecture continues to evolve, one thing is certain: blockchain has moved from the periphery to the mainstream of technological discourse. Whether it fulfills its loftiest promises will depend on how wisely humanity chooses to wield it—but its legacy as a catalyst for a more transparent, decentralized world is already taking shape, block by block.